ANALYSIS: The hidden cost of inaction—brown discounts in CRE

Olga Khroustaleva is co-founder at Building Atlas

Leo (Qizhou) Xiong is partner at Urban Neuron

Introduction: the cost of doing nothing

In the race toward a greener built environment, much of the focus has been on operational energy savings, but there's a silent financial penalty looming for property owners who delay action. This is the brown discount: a measurable decrease in the value or marketability of commercial buildings with poor sustainability credentials, such as Energy Performance Certificate (EPC) ratings.

These lower-rated properties are increasingly being priced down by tenants, investors, and valuers alike. As regulations tighten and market expectations shift, the brown discount is becoming more pronounced, and ignoring it may be one of the most expensive decisions a landlord can make (JLL, 2023).

This analysis explores why brown discounts should be a core input in any cost-benefit analysis of energy efficiency retrofits and not just an afterthought. When properly accounted for, brown discount avoidance plus energy bill savings make a compelling case for proactive investment.

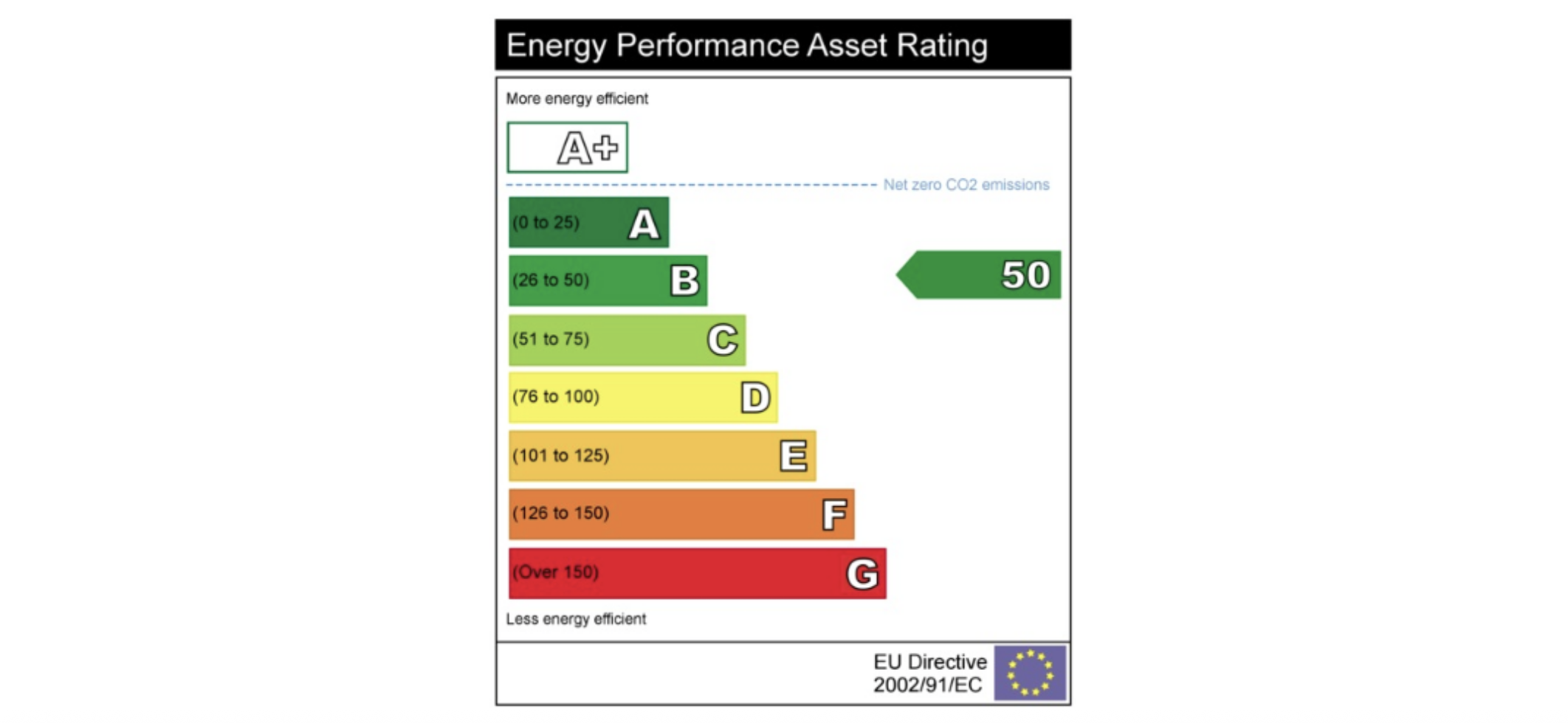

Figure 1: What is a non-domestic Energy Performance Certificate (EPC)?

1. Brown discounts are real and growing

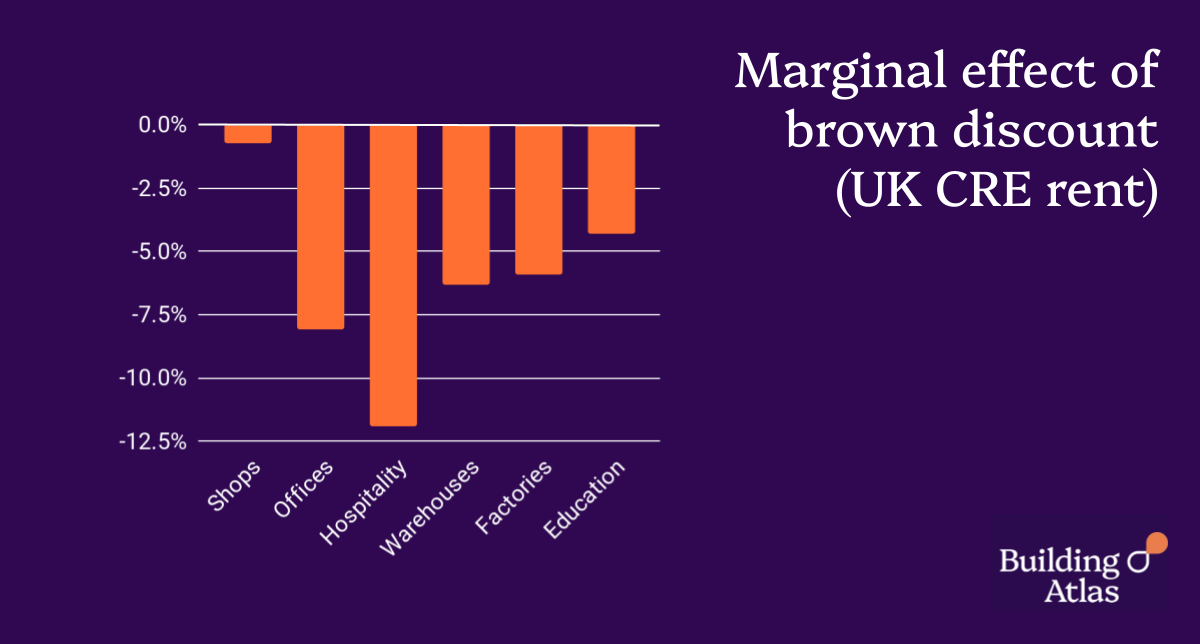

Today’s market increasingly reflects the connection between building efficiency and asset value. Properties with low EPC ratings (E, F, or G) are facing value erosion and leasing disadvantages in both core and secondary markets. JLL has found consistent brown discounts of up to 10–20%, particularly for office and retail assets (JLL, 2023).

Similarly, CBRE reports increasing value divergence between green and brown assets, especially in London and major urban centres (CBRE, 2023; CBRE, 2025). Savills adds that these trends are accelerating ahead of upcoming regulation deadlines (Savills, 2023).

In collaboration with Urban Neuron, Building Atlas has employed the latest Valuation Office Agency (VOA) data and non-domestic EPC data to re-test the theory of brown discount. We found the following strong evidence that brown discounts exist and are largely consistent with the findings from other reports. We define more strictly what would be considered a “brown building” by labelling all non-domestic buildings that have EPC D rating or below as “brown”.

Figure 2: How large are brown discounts?

2. Not all markets are equal: regional variation in discounts

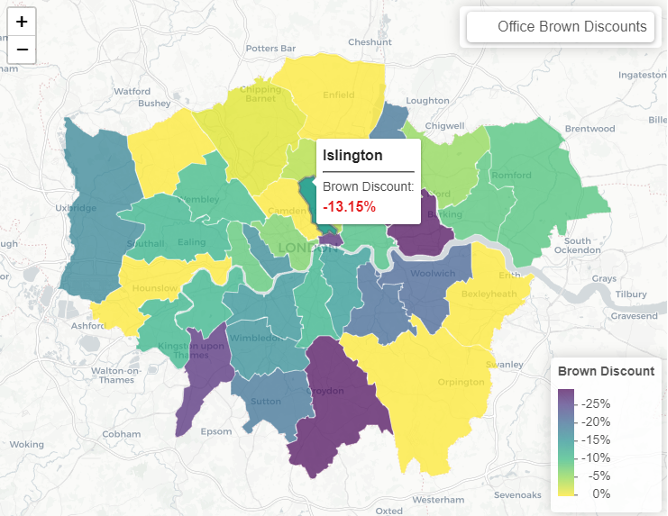

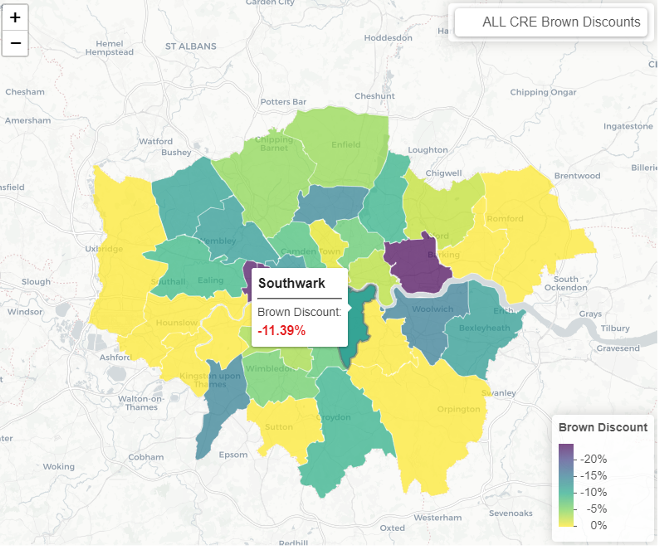

Brown discounts don’t hit evenly across the UK. In higher-demand regions with tighter supply, like central London or the Oxford-Cambridge arc, tenant expectations are stricter, making EPC performance a stronger determinant of rent and capital value (CBRE, 2023). We took a closer look across London boroughs to find that the brown discount varies across boroughs within the Greater London area.

Understanding these geographical dynamics helps portfolio managers focus on retrofit investment where it preserves the most value and reduces future risk. Practically, such guidance on which region suffers the most brown discount allows the investors to maximise the impact of their retrofitting budget.

Figure 3: Brown discounts in office buildings across London boroughs

Figure 4: Brown discounts in all types of CRE buildings across London boroughs

3. The future is green, and the discount will deepen

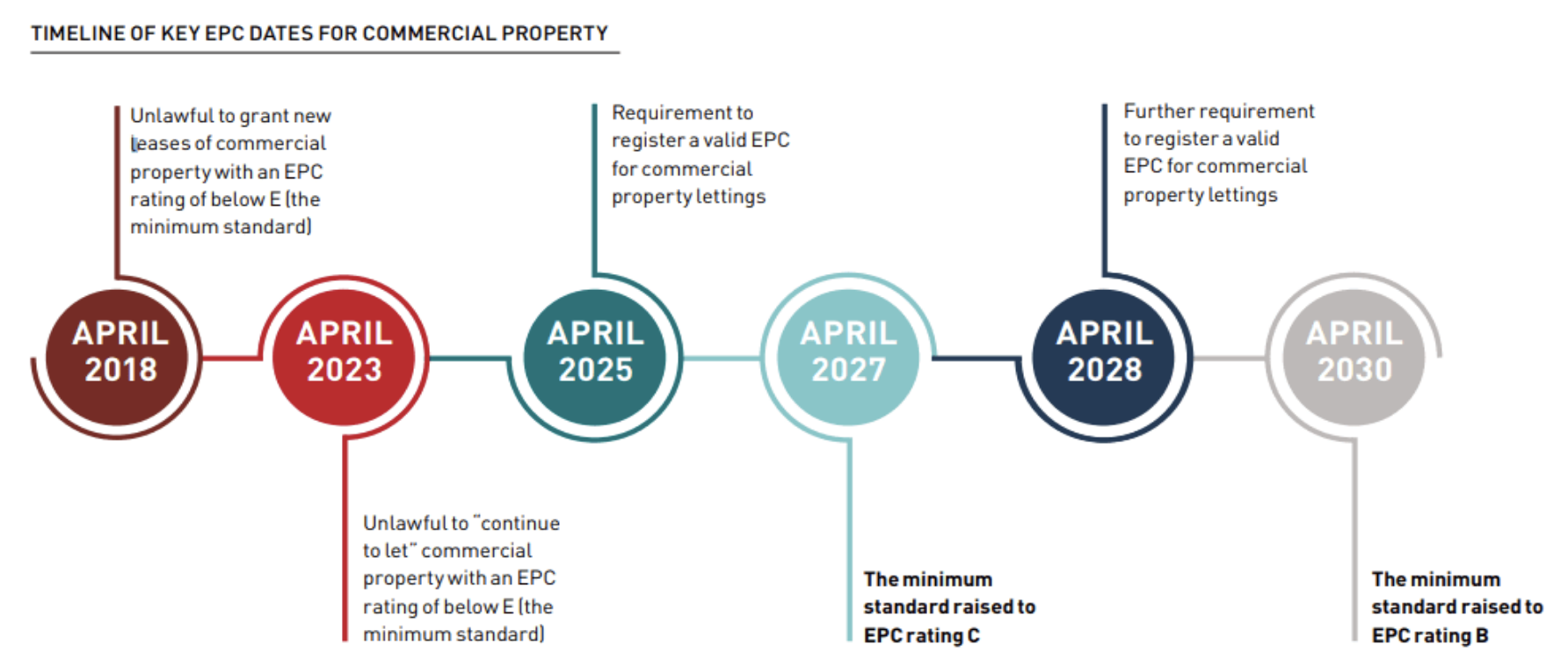

As more buildings improve their energy efficiency and achieve higher EPC ratings, poorly rated assets will become more stranded. The UK’s Minimum Energy Efficiency Standards (MEES) already ban leasing commercial buildings below EPC E, with the bar set to rise to EPC C by 2027 (RICS, 2023). Gradually, regulation will tighten as time progresses and more buildings are upgraded.

When poor energy efficiency buildings become minority offerings on the market, it is highly likely that the brown discount will deepen as they stand out more prominently as the bad players. Moreover, Knight Frank notes that investor due diligence increasingly factors in ESG credentials, further penalising underperforming buildings (Knight Frank, 2024).

Figure 5: Timeline of EPC regulation evolution

4. Retrofitting costs are rising – and so are the stakes

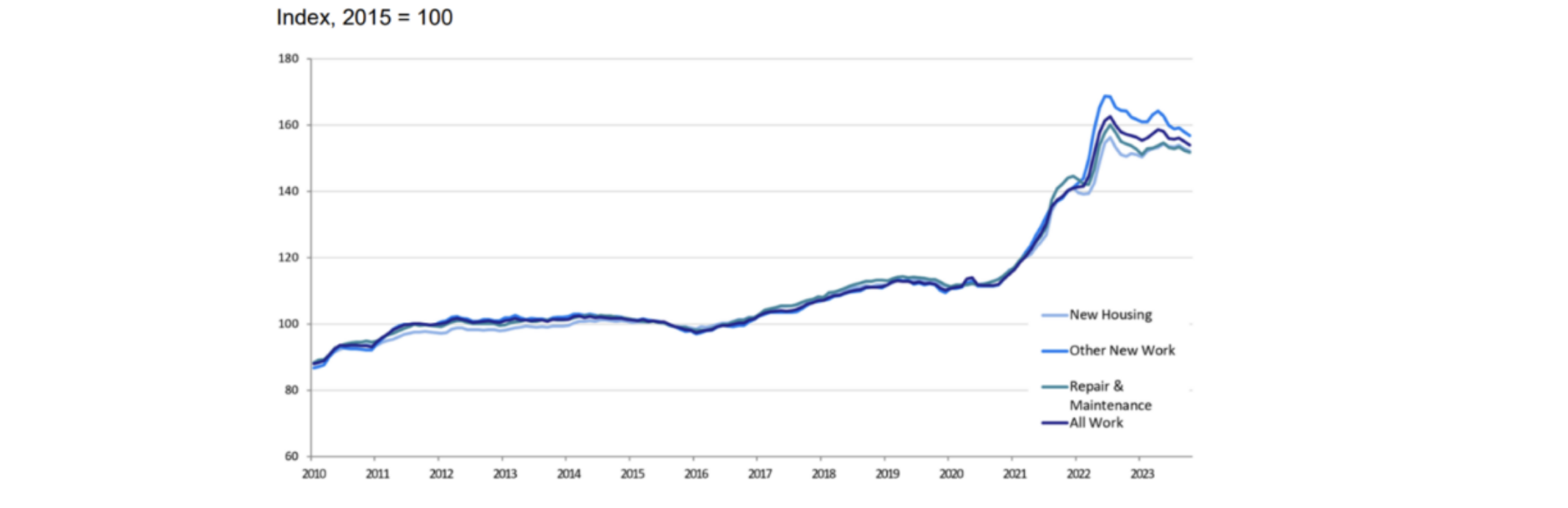

At the same time, retrofitting costs are increasing due to inflation, material shortages, and rising demand for sustainability-aligned contractors. Savills estimates that capital expenditure could rise 15–25% in key components like HVAC, glazing, and insulation by 2026 (Savills, 2023). We have already seen a tremendous increase in construction material costs in the past few years. It is likely that they will remain high and continue to increase.

More importantly, the skilled construction labour shortage in the UK has also pushed up the labour cost of any retrofit project simultaneously. Therefore, delaying retrofit investments could mean higher future costs and lower asset values, a financial double hit.

Figure 6: Construction material price indices, UK

5. Rethinking Retrofit ROI – More Than Just Energy Savings

For years, retrofit projects have been justified almost exclusively by their impact on energy bills, calculating how long it takes for savings to “pay back” the initial investment. But this narrow approach can significantly undervalue the true financial benefit of a retrofit. CBRE and JLL both recommend incorporating this dual benefit approach, showing that ROI can double or triple when brown discount avoidance is included (CBRE, 2023; JLL, 2023).

In a market where buildings with poor Energy Performance Certificate (EPC) ratings face rising valuation pressure, the brown discount avoided must be treated as a critical part of any cost-benefit analysis.

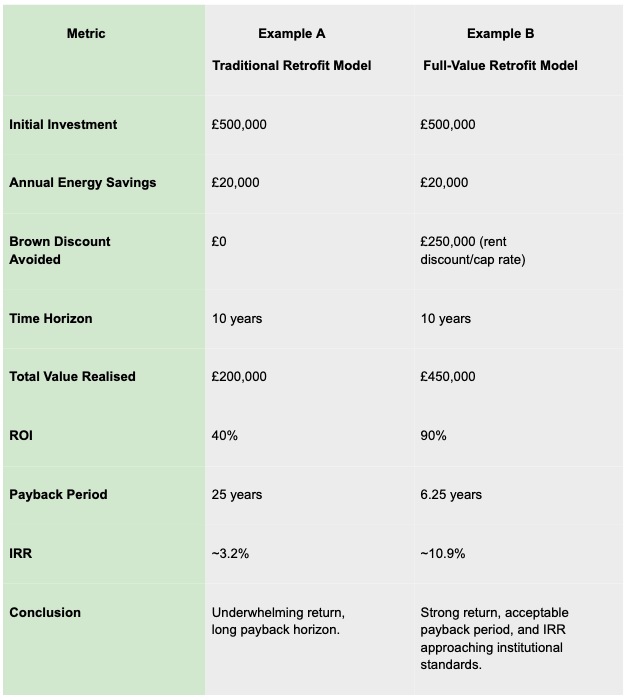

Modern Retrofit Formula: Total Benefit = Energy Savings + Brown Discount Avoided

This expanded view captures not only the operational savings, but the preserved asset value, reduced leasing risk, and future-proofing against regulation.

What these metrics show

Payback period shrinks

When the brown discount is included, the time required to recoup the investment is cut by 75%, a crucial difference for decision makers seeking shorter horizons.IRR increases sharply

The internal rate of return climbs from a marginal 3.2% to a solid 10.9%, now competing with other asset improvement or redevelopment strategies.ROI becomes compelling

A 90% return over 10 years presents a far more strategic use of capital than initially assumed under a traditional view.

Strategic implications

For portfolio managers:

Prioritise buildings where brown discounts are steepest. These are the assets where including this factor in your model will transform the retrofit’s financial case.For capital planners:

Use IRR and payback metrics that account for both risk mitigation and long-term market value, not just OPEX savings.For investors and lenders:

A dual-metric analysis demonstrates stronger stewardship and enhances ESG alignment; a growing focus among institutional capital sources.

Retrofits should no longer be evaluated through a single lens. By incorporating the brown discount avoided into financial modelling, alongside conventional energy savings, stakeholders can capture the full strategic value of these investments. Retrofit projects don’t just reduce carbon. They preserve capital, protect against regulatory risk, and future proof portfolio performance.

Table 1: Scenario Comparison: Traditional vs. Full-Value Model

Conclusion: the time to act is now

The brown discount is no longer hypothetical – it's shaping asset values today and will continue to deepen as the market becomes more sustainability-driven. Retrofitting is not just an environmental obligation; it’s a financial strategy to preserve asset value and marketability.

By including brown discount avoidance in cost-benefit analysis, stakeholders can make smarter, more future-proof investment decisions. The opportunity is clear – act now, or risk falling behind.

References

JLL (2023). The Impact of EPC Ratings on Commercial Real Estate Values. https://www.jll.com/en-de/insights/the-commercial-case-for-sustainable-buildings

CBRE (2023). The Value of Sustainable Building Features https://mktgdocs.cbre.com/2299/ac2eabbf-b83c-417e-8207-b45ce5f48956-703474608.pdf

CBRE (2025). UK Sustainability Index Results to Q4 2024 https://mktgdocs.cbre.com/2299/5349bb8d-a739-4cba-9451-0e3c458dfd15-908628925/UK_Sustainability_Index_Result.pdf

Savills (2023). EPC ratings and planning policy: A comparative analysis across London. https://www.savills.com/blog/article/347511/residential-property/epc-ratings-and-planning-policy--a-comparative-analysis-across-london.aspx

RICS (2023). Sustainability and Commercial Property Valuations. https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/sustainability-and-commercial-property-valuation

Knight Frank (2024). How does ESG impact commercial property valuations? https://www.knightfrank.co.uk/blog/2024/04/09/how-does-esg-impact-commercial-property-valuations

Olga Khroustaleva is co-founder at Building Atlas

Leo (Qizhou) Xiong is partner at Urban Neuron